New light-vehicle sales remained strong in May but fell slightly from April’s highs. May's SAAR totaled 17 million units, as April’s SAAR was revised upward to 18.8 million units. May 2021’s SAAR was up 40.3% from May 2020’s, when light-vehicle sales had just begun to turn around from April 2020’s pandemic lows. In a normal year, a 17 million-unit SAAR would be considered quite solid. But given current market conditions, May’s drop in sales highlights the effects of a supply and demand imbalance.

May 2021 began with total inventory of 1.97 million units, down 17.9% from the beginning of April 2021 and off 39.6% from the start of May 2020. Inventory has been especially constrained in some of the hottest market segments and among the most popular models. Pickups, which were in high demand throughout the past year, represented just 16.6% of new vehicles sold in May 2021, the lowest market share for the segment since March 2019.

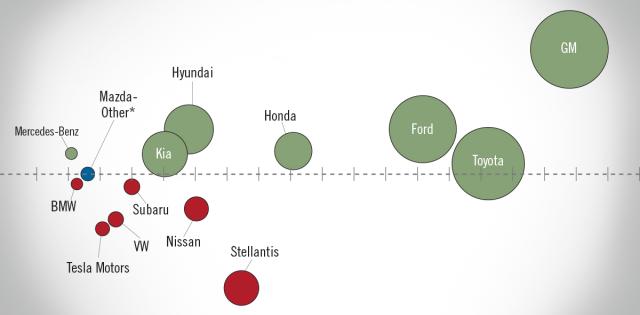

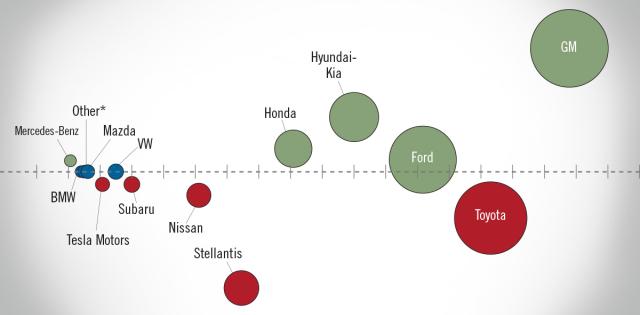

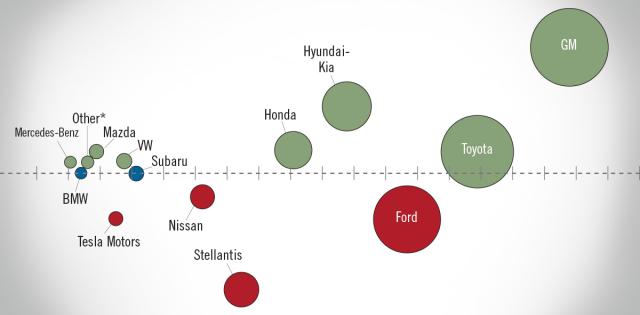

But car market share posted its first year-over-year gain since December 2012, rising to 24.2% from 23.1%—another sign that customers may be settling for second- or third-choice vehicles when unable to find a vehicle in their preferred segment. Many dealers have encouraged customers to place orders for the exact vehicle they want if it’s not available on the lot. As a result, many new vehicles arriving at dealer lots have already been sold, and the ones that aren’t spoken for aren’t available for long. According to J.D. Power, 33.4% of vehicles sold in May 2021 sat on the lot less than 10 days, up from 18.2% in May 2019.

OEMs continued to prioritize deliveries to retail customers over fleet customers. Fleet deliveries accounted for just 10% of new-vehicle sales in May, after averaging 16% in the first four months of the year. Before the pandemic, fleet shares were typically closer to 20% of monthly sales. Even with OEMs prioritizing retail deliveries, retail demand has been very robust, with many reports of the most popular models selling at or above MSRP. With such strong demand, OEMs pulled back incentive spending further in May. Average incentive spending per unit, says J.D. Power, is expected to total $2,957—down from $4,825 in May 2020 and $3,878 in May 2019.

With no end in sight for the supply shortage as sales volumes outpace new-vehicle production, June will likely be a tough month for many dealers. Vehicle production probably won’t improve significantly until later this summer, as supply shortages persist for the rest of the year. Still, we remain confident that new-vehicle demand will continue to be solid through year-end.