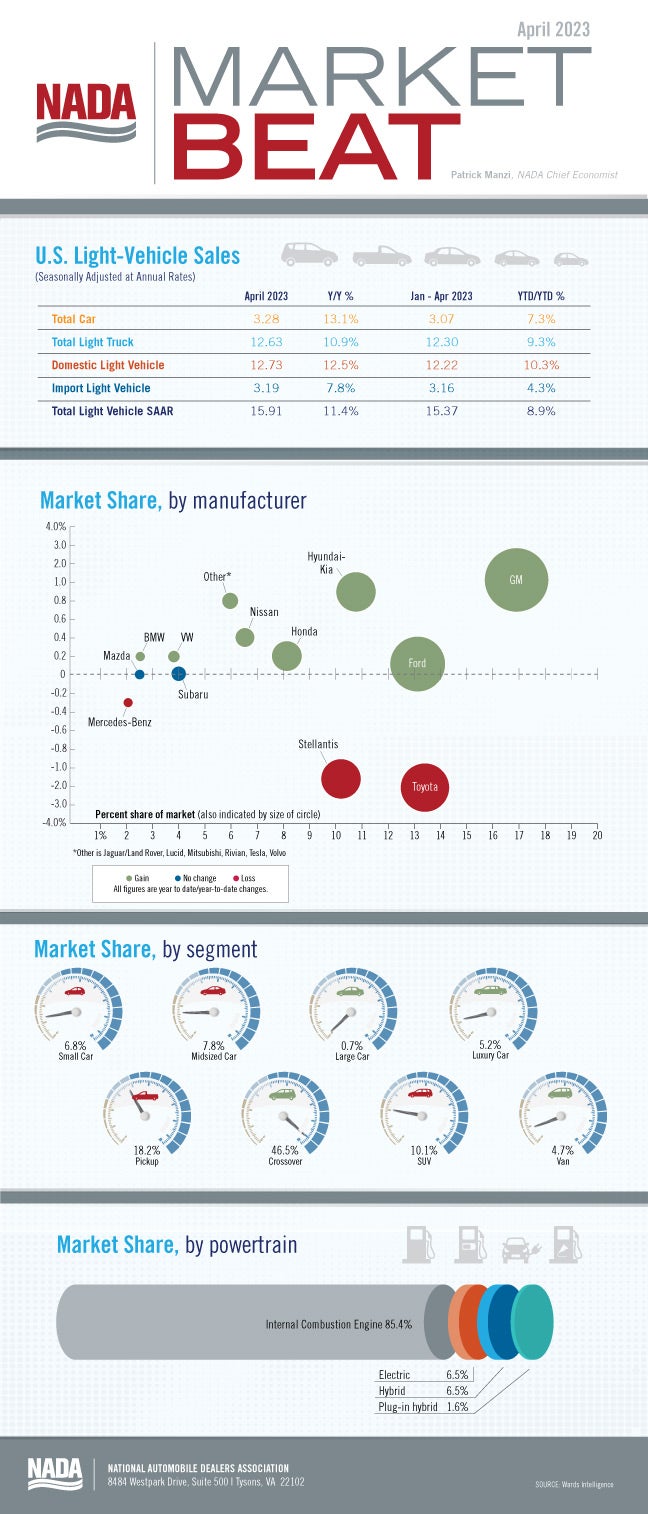

New light-vehicle sales in April 2023 rose significantly year-over-year. The 15.9 million unit SAAR for April 2023 represents an increase of 11.4% compared with a 14.3 million SAAR for April 2022. Increased vehicle availability, which alleviated some consumer and fleet pent-up demand, helped fuel the sales rise. According to Wards Intelligence, fleet sales are forecast to account for 16% of April 2023 sales.

An increasing number of new-vehicle incentives also contributed to the April sales gains. According to J.D. Power, average incentive spending per unit in April is expected to total $1,599, an increase of 58.9% compared with April 2022. While average incentive spending has risen from rock-bottom lows, it has not increased equally for all OEMs. Some OEMs have been able to substantially boost new-vehicle supply, but others are still struggling with vehicle production. Those OEMs with more supply will be better able to offer incentives, and some may even participate in Memorial Day discounting later this month.

Average interest rates and transaction prices remain high and continue to keep new-vehicle monthly payments elevated. According to J.D. Power, the average interest rate on a new-vehicle finance contract in April 2023 is expected to be $729, an increase of $48 year-over-year. The average interest rate on a new-vehicle finance contract should reach 6.8% in April 2023, or 227 basis points higher compared with April 2022. Interest rates will likely climb a bit more, as the Fed is expected to increase rates at its meeting this week.

Looking ahead to the rest of the year, we expect continued sales improvement driven by greater vehicle availability as more OEMs move past the chip shortage. Our forecast for 2023 is 14.6 million units.

For more stories like this, bookmark www.NADAheadlines.org as a favorite in the browser of your choice and subscribe to our newsletter here: