The article below is sourced from Bloomberg Wire Service. The views and opinions expressed in this story are those of the Bloomberg Wire Service and do not necessarily reflect the official policy or position of NADA.

US auto sales likely rose in December and will rebound in the new year as a recovery in vehicle production will more than offset the effects of inflation and rising interest rates.

Two years of semiconductor shortages and supply problems have kept vehicle production low and inventories lean. With factories picking up pace again, consumers will buy more vehicles this year even if automakers have to help them manage rising interest rates by cutting today’s lofty prices.

“We are still seeing strong demand for our vehicles, but we’re mindful because the steady rise of average transaction prices is starting to come back a little,” General Motors Co. Chief Executive Officer Mary Barra said at an Automotive Press Association event in December.

The net effect is that the US auto industry is expected to grow by more than 1 million vehicles in 2023 to about 15 million units. That’s below recent years when automakers enjoyed sales of 16 to 17 million vehicles but signals that the industry can weather this year’s expected economic stress.

“We’re planning for an industry around 15 million,” Barra said, “but having contingency planning plus or minus off of that.”

Retail sales of new cars in December likely rose 4% from a year ago to 1.27 million as inventories continued to improve, according to researcher Cox Automotive. Still, that’s short of the typical 1.5 million units seen in December, when carmakers push year-end sales campaigns to hit annual targets.

Total sales for 2022 were likely below 14 million units, the lowest since 2011, when the US was climbing out of the depths of the Great Recession.

Pent-up Demand

Inflation and interest rates are squeezing some shoppers out of the new-car market and pushing up auto-loan defaults. Meanwhile used-car prices, which determine the trade-in values that many consumers use as currency when buying a new car, are falling.

That won’t deter many new-car buyers, said Jack Hollis, Toyota Motor Corp.’s executive vice president of sales for North America. He said vehicle shortages of the past two years have kept between 4 million and 7 million consumers from buying and many could be back in showrooms this year.

“It’s clear that demand is still outstripping supply,” Hollis said in an interview last month. “Prices keep rising. We will have another year with a supply-constrained sales number.”

Hollis is betting the industry will reach 15 million vehicles this year and could sell as many as 17 million if it weren’t for supply-chain issues.

Carmakers likely sold new cars at an annual pace of 13.2 million in December, up 6% from a year earlier, according to the average forecast of seven market researchers. Most automakers will report their latest quarterly and annual US new car sales on Jan. 4.

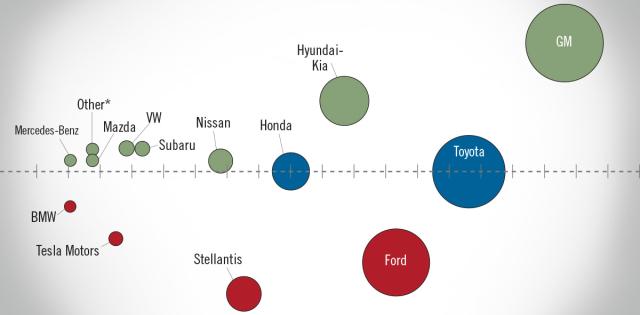

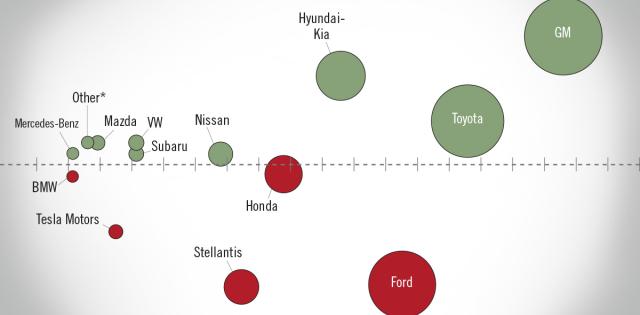

GM, Hyundai Motor Co. and Toyota likely saw big sales gains in December, while deliveries at Ford Motor Co., Stellantis NV, Honda Motor Co. and Nissan Motor Co. dropped versus a year ago, according to RBC Capital Markets analyst Joseph Spak.

While two years of tight inventory may create a floor for demand in 2023, carmakers’ days of minting money on a small volume of vehicles at inflated prices may be waning.

Tesla Inc. this week reported record deliveries but missed analysts’ estimates for the fourth quarter and came up short of its own targeted growth rate of 50% despite dropping prices.

Scott Kunes, chief operating officer of Kunes Country Auto Group, which sells brands from all three Detroit automakers and a host of imports at 43 dealerships across the Midwest, said December was weaker than usual because manufacturers were tight-fisted with incentives.

“Everybody was used to the new normal, pandemic normal where incentives weren’t there because demand was so high and supply was so short,” Kunes said by phone. “We see this abrupt slowdown in demand — I didn’t think it would happen quickly, but the Fed raised rates as much as they have and consumer confidence is pretty down right now.”

The industry’s shift toward building high-margin trucks and SUVs has shrunk the pool of buyers who can afford a new car, he said. Prices are dropping on high-end vehicles, while demand for entry-level cars in the used market is still hot.

Warning Signs

Researcher Evercore ISI expects to see “pricing levers pulled for the first time in two years” in 2023, with sticker prices coming down $1,500 to $2,000 per car, according to a Dec. 23 research note. Dealers will first have to halt their mark-ups before automakers’ profit margins will be affected, the analysts wrote.

One bright spot this year will be fleet sales, thanks to the Inflation Reduction Act. President Joe Biden’s sweeping climate bill grants a $7,500 tax break for electric work trucks, rental cars and delivery vans.

The CEOs of Ford, GM and Rivian Automotive Inc. have all crowed about their expectation for robust commercial vehicle sales as businesses and local governments seek to take advantage of the EV subsidy.

That will mark a reversal of the past two years, when chip scarcity forced automakers to curb their fleet sales to prioritize more profitable retail customers.

(By Gabrielle Coppola with assistance from Ana Monteiro)

For more stories like this, bookmark www.NADAheadlines.org as a favorite in the browser of your choice and subscribe to our newsletter here: