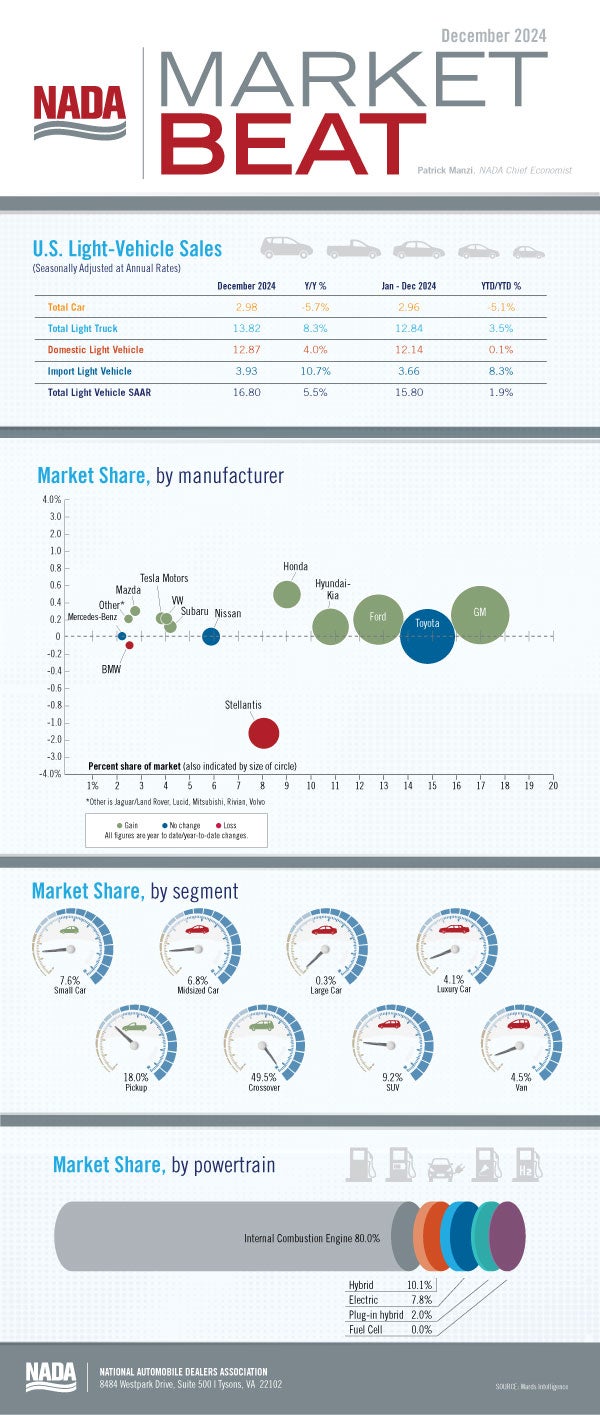

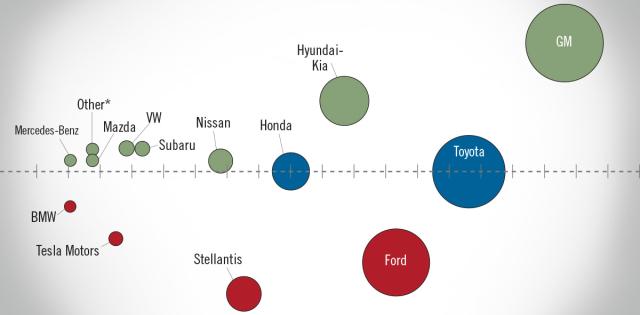

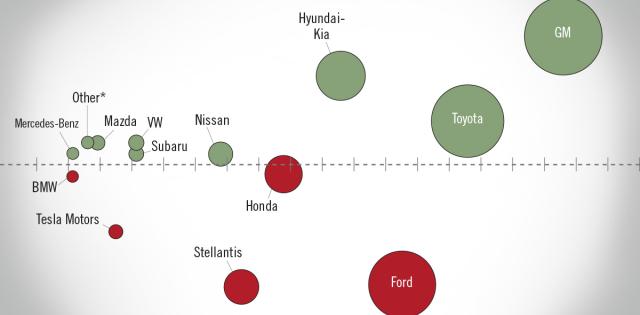

New light-vehicle sales finished the year strong in December, leading to a full-year sales total of 15.85 million units—an increase of 2.2% compared to 2023. The December 2024 SAAR reached 16.8 million units, the highest monthly SAAR since May 2021 with 17.0 million units. New-vehicle sales saw year-over-year gains in the first quarter, followed by declines in the second quarter. New light-vehicle sales accelerated following the election in November 2024 and were strong through the remainder of the year. Sales in Q4 of 2024 totaled 4.19 million units, an increase of 7.7% compared to Q4 of 2023. Significant drivers of the sales gain included higher OEM incentives and increased vehicle availability.

All segments of alternative-fuel vehicles posted year-over-year sales and market-share gains. In total, alternative-fuel vehicles represented 20.0% of all new vehicles sold. Conventional hybrids had the largest increase in market share, rising to 10.1% from 7.6% last year. Plug-in hybrids (PHEV) and battery electric vehicles (BEV) also gained market share, but to a lesser extent. PHEV market share rose to 2.0% in 2024 from 1.9% in 2023, and BEV market share rose to 7.8% in 2024 from 7.5% in 2023. BEV sales reached a record 1.24 million units, an increase of 6.8% year over year. The share of BEVs sold by franchised dealers increased as well, with franchised dealers selling nearly 599,000 BEVs—or 48.1% of all BEVs sold. We expect franchised dealers to capture an even larger share of the BEV market in 2025.

New light-vehicle inventory on the ground and in transit in December 2024 totaled 2.79 million units, down 5.9% compared to the beginning of the month and up by 21% year over year. As new light-vehicle inventory increased through 2024, so did OEM incentives. J.D. Power estimates the average incentive spending per unit in December 2024 was $3,442, an increase of $809 year over year. We expect new light-vehicle production to slow somewhat in 2025, which will limit inventory growth and keep inventory levels just below 3 million units for most of the year.

Looking ahead, there will be challenges for the U.S. auto industry. A proposed rollback or elimination of the consumer-facing electric vehicle tax credits will likely slow BEV adoption and limit sales growth. The Fed has signaled it will slow the cadence of cuts to the federal funds rate. Interest rates declined slightly during the final quarter of the year, which contributed to the strong sales pace in Q4. There certainly will be other challenges as well, but overall, our outlook is positive. We expect continued growth in vehicle sales in 2025. Our forecast for new light-vehicle sales in 2025 is 16.2 million units, an increase of roughly 2% compared to 2024.

NADA Market Beat: Sales Finish Year Strong with Highest Monthly SAAR since May 2021

Published

Share

Author

Image

Image